Own Land? Here’s How I Actually Got a Home Construction Loan

When I bought my land, it didn’t look like “future equity” or “collateral.” It was just rutted soil, scrub grass, and a tired wire fence. I remember standing there thinking, How is this empty lot ever going to convince a bank to give me money?

If you’re in that same spot – you’ve got land, a rough idea of a house, and no idea how to turn it into an actual construction mortgage – this is the path I walked. What worked, what hurt, and what I’d do differently if I started tomorrow.

This isn’t theory. This is the real process I went through to build a house on my own land and get a lender to come along for the ride.

What a Construction Mortgage Feels Like in Real Life

On paper, a construction mortgage is simple. It’s a short-term loan that funds the build in stages, you pay interest only while you’re under construction, and then it turns into a normal mortgage once the house is done.

Living through it is different. It feels more like this:

- The bank doesn’t just look at you. They look at your land, your plans, your builder, and your numbers as one story.

- You don’t get a big lump sum. Funds come out in stages called “draws” after you hit specific milestones.

- You make interest-only payments on what has actually been advanced, not on the total approved amount.

- Your phone learns the rhythm of the project: builder, lender, inspector, repeat.

Think of it this way: the bank is betting that you can turn dirt into a finished house without running out of money or patience. The more you show them you’ve thought this through, the easier everything gets.

If you want a more technical breakdown later, I’ve got a separate explainer on construction mortgages and how they differ from regular home loans in how construction mortgages let you build instead of buy. For now, stay with the story.

Things No One Tells You About Construction Loans

The bank will show you a neat brochure and a perfect draw schedule. Real life is messier. Here are the parts I only learned while building on my own land.

Your land can act like cash (if you set it up right)

If you already own the land, the lender can treat that equity like part or all of your down payment. But they do not care what you paid. They care what it appraises for today and how clean the title is.

On my build, the land was free and clear. The appraiser valued it higher than what I had paid years earlier. That extra value reduced the cash I had to bring in. No one at the bank volunteered that. I had to ask, “Can my lot count as equity in the deal?”

The lender “stress-tests” you quietly

You will see one interest rate on the sheet. Behind the scenes they often test your budget at a higher rate. They want to see that you can still carry the payment if rates jump before the house is done.

That means your own stress test has to be even tougher. Run numbers at a rate or two above what they quote. If the payment already makes your stomach tight at today’s rate, you are too close to the edge for a build.

Draw schedules are more negotiable than they look

The first draft of the draw schedule is usually built for the lender, not for the site. It might release a big chunk way too late, after you have already paid trades out of pocket.

I learned to sit down with my builder and redraw the schedule in simple language: “Foundation poured and inspected,” “shell complete and watertight,” “rough-ins done,” “drywall up,” “finishes.” Then we pushed the lender to align draws with those real milestones.

You do not need a fancy spreadsheet. You just need to make sure the cash shows up roughly when money leaves your pocket.

Inspectors work for the lender, not for you

During construction, the bank will send inspectors before each draw. They are not doing a full quality check. They are just confirming that the work claimed is actually there.

On one of my draws, the inspector showed up, snapped a few photos, and left in five minutes. That’s when I understood I needed my own eyes on the job. Walk the house after each major stage. Look for leaks, sagging, missing flashing, wrong window sizes, bad framing. Fixing problems after drywall is painful.

The “interest-only” phase tricks a lot of people

During the build you usually pay interest only on whatever has been advanced. Those payments can feel tiny at first. Easy to carry. Almost relaxing.

Then the house finishes, the loan converts to a normal mortgage, and the payment jumps. I treated the interest-only phase as rehearsal. I paid extra every month, aiming at what my full mortgage payment would be. That way there was no shock at the end.

Change orders kill budgets faster than lumber prices

Everyone worries about lumber and concrete going up. What actually blew up my spreadsheet was all the “while we’re at it” changes. Bigger windows. Better siding. Upgraded HVAC.

Every change order means more cost and sometimes another appraisal review. I started using a simple rule: no change over a set dollar amount unless we slept on it for 48 hours. That alone saved thousands.

Self-builds scare lenders, but there are ways to calm them down

If you act as your own general contractor, the bank sees more risk. They worry about half-finished houses and blown schedules.

What helped was treating the lender like a partner, not a vending machine. I brought a real schedule, trades lined up, written quotes, and proof I had done similar work before. I also kept a cash cushion outside the project. That showed them I could handle surprises without walking away.

Your time is part of the budget, even if no one writes it down

Nights on site. Weekend runs to the lumber yard. Emails to engineers. None of that shows up in the contract price, but it is real.

Before you sign anything, ask yourself a simple question: “If this build eats most of my evenings and weekends for a year, is it still worth it?” If the honest answer is no, scale the project back or delay it.

A construction loan is just a tool. Used right, it turns a bare piece of land into a house that actually fits your life. Used blindly, it can trap you in a project that runs your money and your nerves dry. The difference is how much you plan before the first shovel hits the dirt.

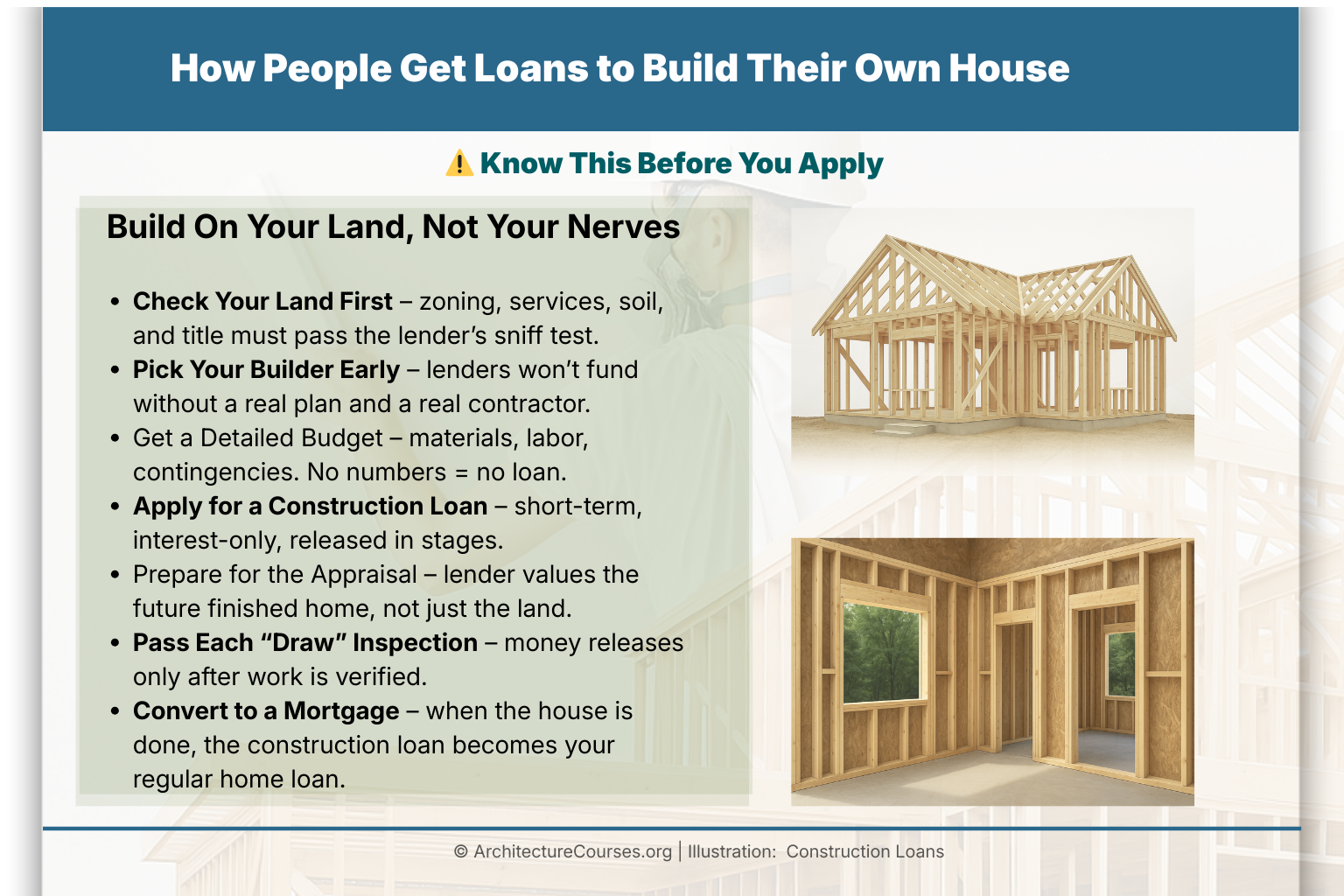

Step 1 – Make the Land “Bankable” Before You Talk Money

I assumed that owning land was enough. It isn’t. The bank wants to know if that land is actually buildable, legal, and simple enough that the project won’t die halfway through.

Check title and clear out any land drama

The first thing the lender did was pull title. They wanted to see:

- No surprise liens hanging off the property.

- No bizarre easements cutting through the middle of the lot.

- My name clearly on title, not “almost” or “in progress.”

I had a real estate lawyer do a clean title check before I even booked a meeting with the bank. It cost a bit, but it meant I wasn’t blindsided later by old paperwork.

Walk into the planning office with your ego in your pocket

Next, I took my rough sketch and lot info down to the planning department. I didn’t show up as “future architect of my dream home.” I showed up as “person who doesn’t want to be told no later.”

The planner pulled the zoning map and walked me through the boring but important stuff:

- Setbacks from property lines.

- Height limits and coverage percentages.

- Driveway rules, corner lot rules, and all the little “bylaws” nobody reads until they’re in trouble.

At one point they drew a thick line on my sketch and said, “You can’t build past here.” That single line changed my floor plan and probably saved me months of permit delay.

Know your services and access before you brag to the bank

The lender also cared about basics that don’t feel exciting when you’re dreaming about kitchens:

- Is there legal, year-round road access?

- Are you on city services, or do you need well and septic?

- How far do power, gas, and other utilities need to travel?

On my build, the driveway and service trench ended up being a bigger line item than I wanted to admit at the start. Once I accepted that and folded it into the budget, the land started to look “bankable” instead of “cheap but complicated.”

If you’re still at the “raw land, rough dream” stage, read through how to get a loan to build on land you already own as well. It forces you to deal with the boring pieces early, which is exactly what lenders want to see.

Step 2 – Turn the Dream House into Real Plans and Numbers

The bank doesn’t finance wishlists. They finance plans, contracts, and budgets that look like someone has already done half the risk work for them.

Get real drawings, not napkin sketches

I started with graph paper and scribbles. That was for me. What the lender wanted to see was:

- Full floor plans and elevations.

- Basic structural information and roof layout.

- Enough detail that an appraiser could put a value on the finished house.

Once the drawings were far enough along, pricing suddenly got more honest. We could talk about actual window sizes, real spans, and the difference between “simple roof” and “that will cost you.”

If you feel fuzzy on how a house frame actually comes together, it’s worth reading something like House Framing 101. Knowing how studs, plates, and sheathing really work makes it easier to see where the money actually goes.

Pick your builder and contract type with your lender in mind

I talked to a few builders. Some were cheap and chaotic. Some were expensive and organized. The lender gently nudged me toward a fixed-price contract with someone who had a clean reputation.

Here’s how the options looked from my side:

- Fixed-price contract: One number for the build. Changes cost extra. The builder owns their estimating mistakes.

- Cost-plus: You pay actual costs plus a fee. Transparent, but you carry the risk if prices spike or something goes sideways.

The bank was blunt: a fixed-price contract made them more comfortable, especially for a first build. So that’s where I landed. We still built in a contingency, but we weren’t guessing line by line.

Build a real budget and a real contingency

At the beginning, I lied to myself. I had a number in my head that felt “reasonable,” and I kept trying to force the build to fit it. It never does.

The budget that finally worked included:

- Land and site work.

- Foundation, framing, roof, and exterior envelope.

- Mechanical systems – electrical, plumbing, HVAC.

- Interior finishes and a modest landscaping allowance.

- A contingency fund of at least 10–15% for surprises.

That contingency saved me more than once: rock in the wrong place, inspector asking for extra waterproofing, a couple of finish upgrades we decided were worth it once we saw spaces in person.

Step 3 – Choosing the Type of Construction Loan

Once the plans and budget were in good shape, the next decision was the loan structure itself. This is where a lot of people get stuck in analysis mode. I did too.

Construction-to-permanent (what I used)

I went with a construction-to-permanent loan, sometimes called “single-close.” You close once, build the house, and then the same loan converts into a regular mortgage at the end.

During construction, I paid interest only on what had actually been advanced. Once the house was finished and signed off, the loan flipped into a standard mortgage with principal and interest.

Why I liked it:

- One closing, one set of legal fees.

- I had a clear idea of my long-term payment from the start.

- I didn’t have to go shopping for a new lender while drywall dust was still in my hair.

Construction-only (why I skipped it)

The other option was a pure construction loan that would run for 6–18 months. At the end, I’d refinance into a separate mortgage.

That route can make sense if you’re sure you’ll get a better long-term mortgage later, or if a local lender is great at construction financing but not great at regular mortgages. In my case, the double closing costs and uncertainty just weren’t worth it.

Owner-builder loans (the tempting but tough option)

I flirted with the idea of going full owner-builder. I like tools. I like schedules. I like the idea of saving on contractor markups.

My lender liked the idea much less than I did.

With owner-builder loans, the bank starts asking different questions:

- Have you run a build before?

- Do you understand permits and inspections?

- Do you have trades lined up who trust you?

They may still lend, but often on tighter terms. More down payment, more questions, and more checking in. I decided I had enough to learn on one project and hired a builder, then did smaller chunks of work myself where it made sense.

Step 4 – What the Bank Actually Needed from Me

By the time I sat down for the real application, my folder was thick enough to feel like a university thesis.

Your financial picture on the table

The lender went deep on my numbers:

- Credit score and history.

- Debt-to-income ratio.

- Existing loans, cards, and obligations.

They weren’t just looking for perfection. They were looking for stability. Construction is messy by nature. They want to know you can handle a messy year without missing payments.

Land equity and down payment

Because I already owned the land, part of my “down payment” was already sitting in the dirt. The bank ordered an appraisal, looked at what I owed on the lot, and treated some of that equity as my contribution to the project.

On top of that, they still wanted cash. Enough to show I could cover closing costs, interest during construction, and the early stages before the first draw came through.

The builder package

On the construction side, they wanted:

- Signed building contract.

- Cost breakdown by trade.

- Builder’s license and insurance info.

- A history of finished projects, not just promises.

One underwriter actually commented on my builder’s reputation. That told me a lot. The bank is not only lending to you. In a quiet way, they’re also “lending” to your builder’s process.

Step 5 – Living with the Draw Schedule

Getting approved felt like a win. But the real rhythm started when the first excavator bucket hit the ground and the draw schedule kicked in.

How the draws were broken up

Your exact stages will depend on your lender and your region, but my draws looked roughly like this:

- Foundation: Land value plus excavation, footings, and foundation done.

- Lock-up: Framing, roof, windows, and exterior doors in – house weather-tight.

- Rough-in: Electrical, plumbing, HVAC rough-in complete, insulation and drywall up.

- Finishes: Kitchen, baths, and most interior finishes installed.

- Completion: Final inspection and occupancy.

Before each draw, my builder submitted an invoice and a simple progress summary. The bank sent an inspector, I paid a small inspection fee, and then the funds were released.

Cash flow and patience

The friction comes when scheduling gets tight. Trades want deposits. Weather delays an inspection. An appraiser is booked out for a week.

What helped me:

- Keeping a small personal buffer so I could float deposits if a draw lagged a few days.

- Communicating clearly with the builder about when money would arrive, not “soon.”

- Not stacking too many trades on top of each other in the same week right before a draw.

The construction loan isn’t just about big numbers. It’s also about managing lots of small timing details without losing your mind.

Step 6 – The Mistakes I Almost Made

Looking back, the project didn’t go perfectly. It went “well enough,” and that’s usually what a real build looks like. Here are the big near-mistakes.

Trying to squeeze the budget into a fantasy

At first, I kept trying to force the build into a number that was simply too low for what I wanted. Every time we cut something, I’d quietly add something else back in.

The turning point was being honest about:

- The real cost per square foot in my area.

- What my must-haves actually were.

- What I could live without for a few years if needed.

Once I stopped pretending, the lender relaxed, the builder relaxed, and I stopped waking up at 3 a.m. redoing math.

Underestimating how much the builder’s reputation matters

There was a cheaper builder I almost chose. Nice guy, good talker, thin references. One inspector and one homeowner both gave me that “long pause” when I mentioned his name.

The bank would still have lent, but they made it clear the file would be treated with more caution. That was enough of a red flag. I went with the builder who was a little more expensive and a lot more boring on paper – and that’s exactly who you want running a six-figure project.

Not paying attention to lien rules and holdbacks

Depending on where you live, the lender may automatically hold back a portion of each draw to cover potential construction liens. It’s not optional. It’s built into the legal system.

If you don’t understand that, you can end up mentally spending money that never actually hits your account. You can also end up arguing with trades who don’t understand it either.

A short meeting with a construction lawyer and a blunt talk with my builder about how we’d handle holdbacks saved a lot of drama later.

MUST READ – Books That Helped Me Build Smarter

I’m not a fan of random shopping lists. But a few books honestly earned their place on my build – they helped me understand what was happening on site and pushed me to ask better questions before I signed things.

MUST READ – Framing and Structure

Framing Floors, Walls & Ceilings (For Pros By Pros)

A clear, job-site style walk through real framing work. If you’re going to build on your own land, you don’t need to swing every hammer, but you do need to know what a straight wall, a solid floor, and a proper load path look like.

FIELD PICK – Full House Framing Overview

Complete Book of Framing: An Illustrated Guide for Residential Construction

This one dives deeper into layout, headers, roofs, and all the details that tend to show up as “extras” if you don’t plan for them. The more you understand here, the less likely you are to get surprised mid-build.

RECOMMENDED TOOL – A Nail Gun That Can Actually Keep Up

Metabo HPT Framing Nailer

If you’re taking on any of the framing or heavy carpentry yourself, having a reliable framing nailer is the difference between “small weekend projects” and “actually getting through a wall or two without wanting to quit.”

Use tools and books like these to make yourself a better client and a smarter owner. You don’t need to become your own crew. You just need to know enough that nobody can rush you past important decisions.

Quick Notes by Country (Big Picture Only)

The core logic of construction financing is similar in most places: staged advances, inspections, interest-only during the build, then a regular mortgage. The details live in local rules and bank habits.

Canada

On my side of the border, construction mortgages are pretty common. Banks are used to dealing with draws, progress inspections, and land equity. The climate adds another layer: insulation, windows, and heating aren’t optional luxuries. They are budget drivers.

United States

In the U.S., you’ll find a mix of local banks and credit unions that specialize in construction-to-permanent loans. Some regions are more open to owner-builder setups, others lean hard on licensed contractors. Either way, permits and inspections matter just as much as numbers.

UK, Australia, New Zealand and others

In those markets, planning permission, consents, and local building regulations take center stage. The logic is still the same – staged lending to a finished home – but the paperwork and language change. Always start with local rules before you start sketching the dream house.

If I Had to Start Again from Bare Dirt

If I lost the house but kept the lessons, here’s what I’d carry into a new build on my own land:

- I’d treat the budget and contingency like structural elements, not afterthoughts.

- I’d choose the builder whose past clients talk calmly about them, not the one who just has the lowest bid.

- I’d walk into the bank with a package that feels finished: drawings, contract, budget, timeline, and a clear story.

- I’d keep my personal finances boring and predictable until the house was done and the mortgage was settled.

Building on your own land isn’t a TV montage. It’s mud, inspections, unexpected costs, and a lot of small decisions that add up. But when you finally move into a place that grew out of your own dirt – funded by a construction loan you wrestled into place – it feels different than buying something turnkey.

You don’t just own the house. You know it, from survey stakes to final draw, and that changes how you live in it.

FAQ

1. How is a construction loan different from a regular mortgage?

A construction loan is short term. It releases money in stages as the house is built. You usually pay interest only on what has been advanced. When the house is complete, the loan is either paid off with a new mortgage or converts into one.

A regular mortgage is long term. You get the full amount on day one to buy a finished home and start paying back principal and interest right away.

For a plain language U.S. overview of mortgages and how payments work, see the Consumer Financial Protection Bureau’s “Owning a Home” tools: CFPB – Owning a Home .

2. Can my land count as the down payment for a construction loan?

Often yes. If you own the land, the lender can treat the current appraised value of the lot (minus any liens) as equity in the project. In some cases that covers most or all of the down payment.

Lenders in both the U.S. and Canada will still look at your full financial picture: income, credit, other debts, and total project cost. The land is one piece of the puzzle, not the whole thing.

In Canada, you can use the federal Mortgage Qualifier Tool to see how equity and income might affect what you qualify for: Canada.ca – Mortgage Qualifier Tool .

3. What kind of credit score and down payment do lenders usually want?

Every lender is different, but construction loans are almost always stricter than regular mortgages. In practice, many banks like to see:

- A solid credit score (often in the high 600s or above).

- A down payment in the 20%+ range based on total project cost (land + build).

- A comfortable debt-to-income ratio after the new payment is added.

In Canada, the Financial Consumer Agency of Canada explains how lenders look at income, debts, and the federal “stress test” when deciding if you qualify: Canada.ca – Preparing to get a mortgage .

4. How do draws and inspections actually work?

The lender agrees to a draw schedule: a list of stages such as foundation, framing, lock-up, rough-ins, drywall, and completion. After each stage, they send an inspector or appraiser to confirm the work is done.

Once the inspector signs off, the lender releases the next chunk of money. You use that to pay trades and buy the next round of materials.

In the U.S., the CFPB’s mortgage resources explain how lenders handle inspections and appraisals during complex loans: CFPB – Mortgage process overview .

5. Are there government-backed construction or new-build programs I should know about?

Yes. These programs change over time, but here are a few examples to watch:

- Canada: CMHC offers insured products that can support building or major improvements, such as CMHC Improvement and other homeownership programs tied to new construction. Start at: CMHC – Canada Mortgage and Housing Corporation .

- Canada (planning tools): The federal government also links to CMHC guides and tools from its home-buying hub: Canada.ca – Buying a home .

- United States: Government-backed mortgages (FHA, VA, USDA) sometimes offer construction-to-permanent options through approved lenders. Details are on the official HUD site and the CFPB’s mortgage pages.

Always check the official housing or finance agency in your country. Programs for new builds and self-builds are updated often.

6. I’m in Canada. Where can I run numbers and see if I’m even close to qualifying?

The federal government gives you two useful calculators:

- Mortgage Qualifier Tool to see if your income and debts might support the mortgage you want.

- Mortgage Calculator to test payment amounts, amortization, and prepayments.

These tools do not approve you, but they tell you how close your situation is to what banks usually expect.

7. I’m in the U.S. Where can I get unbiased info on construction and other home loans?

The Consumer Financial Protection Bureau is the federal agency that regulates many mortgage lenders. Their site breaks down loan types, closing costs, and how to compare offers in plain language.

Start with their main mortgage toolkit here: CFPB – Owning a Home . From there you can explore guides on rates, closing disclosures, and questions to ask your lender.

8. What if I’m building in another country like New Zealand or Australia?

The basic construction loan ideas are the same everywhere: staged funding, inspections, and a final shift into long-term financing. What changes are the rules, consents, and local building standards.

For example, in New Zealand you can use the official “Can I Build It?” tool to see if your project needs a building consent: canibuildit.govt.nz – Do you need a building consent? . Local councils then publish step-by-step guides for applying.

In Australia and the UK, state or national government sites offer similar planning and building guidance. Always start with your local government’s building or planning department and then talk to a lender who does a lot of construction loans in your area.